The Sovereign Individual’s Dilemma: How Crypto Declaration Laws Create the Infrastructure for Confiscation

Registration precedes restriction. Restriction precedes confiscation. France’s new crypto declaration mandate isn’t just bureaucracy—it’s following a pattern that has repeated throughout history, most

Reading time: ~15 minutes

Picture this: You’re sitting at your kitchen table, staring at a government form that asks you to list every bitcoin wallet you control. The deadline is approaching. You’re a law-abiding citizen. You’ve never hidden anything from the tax authorities. So you fill it out honestly—wallet addresses, approximate balances, the whole nine yards.

You hit submit.

What you don’t realize is that you’ve just done something that would have been unthinkable to the cypherpunks who created Bitcoin: you’ve turned your private keys into a government registry.

When France mandated that citizens declare their self-custodied cryptocurrency holdings in early 2024, they didn’t just create a new tax form. They weaponized compliance itself, transforming your financial sovereignty into a permission slip that can be revoked with a single legislative vote. And here’s the uncomfortable truth: France is just the beginning.

This isn’t another “government bad, crypto good” rant. This is about a fundamental trap that’s being set—one that most people won’t recognize until it’s too late.

The Compliance Paradox: Playing a Game Where the Rules Change Mid-Match

What happens when you play by rules that someone else gets to rewrite whenever they want?

You lose. Every single time.

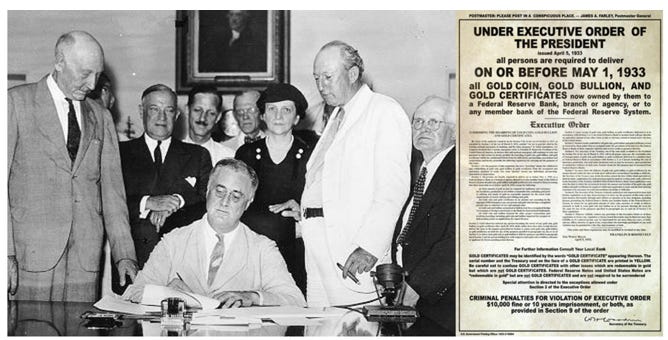

Traditional compliance assumes a stable playing field—you follow the law, the law protects you. But cryptocurrency has exposed something that gold bugs learned the hard way in 1933: when the rules apply to your most valuable assets, “following the law” can become the very thing that destroys you.

April 5, 1933. Executive Order 6102. President Franklin D. Roosevelt didn’t ask Americans to voluntarily surrender their gold. He commanded it. Citizens were required to deliver all gold coins, bullion, and certificates to the Federal Reserve in exchange for $20.67 per troy ounce—a rate set by the government. The penalty for non-compliance? Up to $10,000 in fines (equivalent to roughly $230,000 today) and up to 10 years in prison.

“But that was different,” you might say. “That was the Great Depression. Emergency circumstances.”

Sure. Let’s play that out.

Canada, February 2022. The trucker protests. Under the Emergencies Act, the Canadian government froze approximately 206 financial accounts totaling $7.9 million CAD—including cryptocurrency wallets—without court orders. No trial, no due process. Just a political decision and suddenly your “self-custodied” assets weren’t yours anymore.

India spent years oscillating between extremes. In 2018, the Reserve Bank of India effectively banned crypto by prohibiting banks from dealing with cryptocurrency businesses. The Supreme Court overturned this in 2020. By 2022, the government imposed a 30% tax on crypto gains and a 1% TDS (Tax Deducted at Source) on transactions—policy whiplash that left holders uncertain whether their assets would be legal from one year to the next.

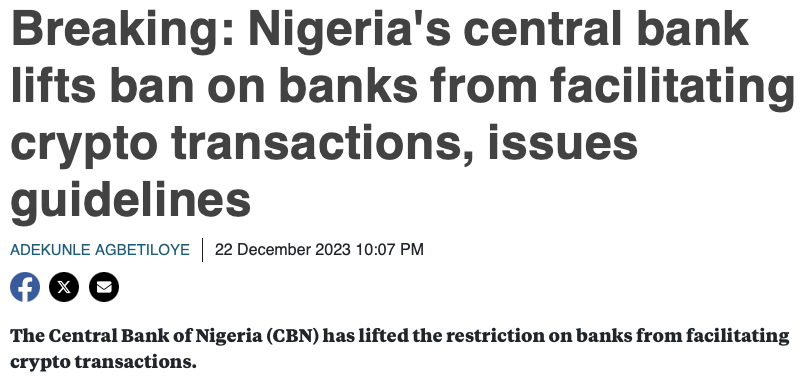

Nigeria banned financial institutions from facilitating cryptocurrency transactions in February 2021, then launched their own central bank digital currency (the eNaira) eight months later. The message was clear: state-controlled digital money is acceptable. Citizen-controlled digital money is not.

See the pattern? Registration is always step one. Restriction is step two. Confiscation is step three.

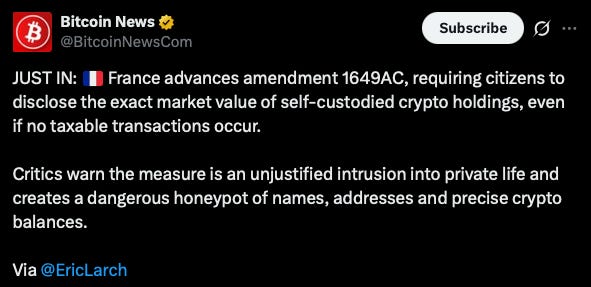

The French mandate isn’t about taxes—not really. France’s 2022 Finance Law requires declaration of digital asset accounts held on foreign platforms and, as of 2024, extends to self-custodied wallets. Failure to declare can result in fines up to €750 per undeclared account, with a maximum penalty of €10,000. It’s about creating a comprehensive database of who holds what.

Once that database exists, it becomes the loaded gun sitting on the table. Maybe nobody pulls the trigger during this administration. Maybe the next one leaves it alone too. But what about the one after that? What about during the next financial crisis, when governments get desperate? What about when your country decides that “economic terrorists” need to have their assets frozen, and your name appears on a list because you donated to the wrong protest or supported the wrong candidate?

You filled out that form honestly because you thought compliance would protect you. It won’t. It’s painting a target on your back.

The Data Security Nightmare: When Your Government Becomes Your Biggest Vulnerability

Let’s talk about something nobody wants to think about: what happens to that database you just populated with your wallet addresses and balances?

If you were a professional cybercriminal, where would you focus your efforts—random exchanges or a government database that literally lists everyone’s holdings with verified identities attached?

Government databases aren’t Fort Knox. They’re more like honey jars with the lids half-off.

In 2015, the U.S. Office of Personnel Management suffered a data breach that compromised the personal information of 21.5 million current and former federal employees—including Social Security numbers, fingerprints, and background investigation records. In 2017, Equifax—a private company handling sensitive financial data with numerous government contracts—exposed the personal information of 147 million people. In 2023, the U.S. saw a 78% increase in data breaches compared to 2022, with 3,205 incidents affecting over 353 million individuals.

These aren’t hypotheticals. These are Tuesday afternoons in the world of data security.

A government registry of cryptocurrency holders is the world’s most valuable target list. It’s like the phone book, except instead of addresses, it’s got wallet balances. Instead of “John Smith, 123 Main Street,” it’s “John Smith, 12.7 BTC, currently worth $850,000.”

In countries with developing cybersecurity infrastructure—which is most of the world—these databases might as well be written in chalk on the sidewalk.

And once your information leaks (not if—when), you’re not just dealing with digital theft. You’re dealing with the very real possibility of physical danger.

In December 2017, Pavel Lerner, founder of the EXMO cryptocurrency exchange, was kidnapped in Kiev and held for ransom. He was released after approximately one week, reportedly after a ransom payment—demonstrating that cryptocurrency wealth makes individuals tangible targets for physical violence.

In 2019, a Norwegian cryptocurrency millionaire was murdered in his home during what police believe was a targeted robbery. Tor Ekeland, a lawyer who represents cryptocurrency clients, told The New York Times: “There’s a big sign on your back that says, ‘Rob me,’ if people know you have a lot of cryptocurrency”.

Industry data confirms this isn’t paranoia. Research from Chainalysis found that in 2023, cryptocurrency theft reached $1.7 billion through hacking alone—not including physical coercion or $5 wrench attacks. When criminals know you hold substantial crypto and know where to find you, the irreversibility of cryptocurrency transactions becomes a feature for criminals, not users.

Your government’s compliance requirement doesn’t protect you. It exposes you.

Unlike a bank account that can be frozen or recovered, cryptocurrency is designed to be irreversible. Once it’s gone—through hacking, coercion, or physical threat—it’s gone. The very feature that makes Bitcoin valuable becomes your greatest vulnerability when someone knows you have it.

You declared your holdings because the government told you to. But who’s protecting you from the consequences?

Self-Custody Without a Trail: The Architecture That Actually Protects You

Here’s where we need to get real about what sovereignty actually means.

Self-custody—holding your own keys—is critical. It’s the foundation. But here’s what nobody tells you: self-custody alone isn’t enough if your name is in a government database next to your wallet address.

Think of it like this: You’ve escaped from prison, but you’re wearing an ankle monitor. Sure, you’re “free”—but they know exactly where you are.

True financial privacy requires breaking the chain between your identity and your holdings. Not to evade taxes on realized gains (that’s illegal, and I’m not advocating for it). But to protect yourself from:

- Future confiscation based on laws that don’t exist yet

- Criminal targeting based on leaked databases

- Political weaponization of financial surveillance

- Gradual erosion of property rights through regulatory creep

The technical architecture of true privacy has three layers:

Layer 1: Self-custody (you control the keys)

Layer 2: Privacy (no one can trace the keys to you)

Layer 3: Operational security (your behavior doesn’t compromise layers 1-2)

Most people stop at Layer 1 and think they’re sovereign. They’re not. They’re just holding their own leash.

The breaking point—the moment you actually achieve financial autonomy—is when you sever the connection between Know Your Customer (KYC) data and your wallet holdings.

KYC was sold as an anti-money-laundering tool. In practice, it’s become a comprehensive surveillance net that turns every exchange into an informant and every transaction into a permanent record. Industry estimates suggest that more than 99% of Bitcoin transactions through major exchanges are now subject to KYC requirements. The surveillance net is nearly complete.

At what point does your personal security outweigh the system’s demand for total transparency?

For many people, that point is now.

The Practical Path: From Exchange to Sovereign Stack

Important disclaimer: This describes technical architecture, not legal advice. Consult a tax attorney in your jurisdiction before implementing any privacy strategy. Laws regarding cryptocurrency, reporting requirements, and privacy tools vary significantly by country. You remain responsible for complying with tax obligations on any realized gains.

Okay, enough philosophy. Let’s talk about what this actually looks like in practice.

You’re not going to completely de-bank and disappear into the forest (though if that’s your vibe, respect). You’re going to use the existing system strategically—taking what you need from it while minimizing your exposure.

Here’s the step-by-step path from KYC-tracked exchange user to genuinely private Bitcoin holder:

Step 1: Acquire bridging assets on KYC exchanges

You start where most people start—on Coinbase, Kraken, Binance, whatever. You buy USDT or another stablecoin. Yes, this transaction is tracked. Yes, your government knows you bought crypto. That’s okay—for now, you’re playing by the rules.

Step 2: Withdraw to a self-custodied wallet

This is where most people stop, thinking they’re done. They’ve “taken custody.” But all they’ve really done is move tracked funds from the exchange’s wallet to their own wallet. The exchange—and by extension, the government—knows that wallet belongs to you.

Blockchain analytics firms can trace approximately 85% of Bitcoin withdrawn from major exchanges to their destination wallets through on-chain analysis. Think of it like withdrawing cash from an ATM. Yes, the cash is now in your pocket. But the bank recorded the withdrawal, the ATM cameras saw your face, and your account statement shows exactly how much you took out.

You’ve broken the first link in the chain. But the chain isn’t broken yet.

Step 3: Privacy-preserving swaps to break the chain completely

This is where the magic happens—and by magic, I mean mathematics and cryptographic protocols.

You use a privacy-focused swap service to exchange your USDT for BTC. But here’s the critical difference from a regular exchange: the swap happens without creating a traceable link between your KYC identity and the resulting Bitcoin.

Imagine you’ve got a dollar bill with your name written on it. You walk into a crowded room, put it on a table with hundreds of other bills, everyone shuffles them around, and you pick up a different dollar bill—one with no name on it. You still have a dollar. But nobody can prove which bill you took or where it came from.

That’s essentially what privacy-preserving swaps do with your crypto. The technical mechanism varies—some services use CoinJoin protocols that mix multiple users’ transactions together, making it computationally infeasible to determine which input corresponds to which output. Others use atomic swaps across different blockchains, severing the direct on-chain connection.

The USDT goes in from your known wallet. BTC comes out to a completely fresh wallet that has no connection to your identity in the KYC database.

The exchange knows you bought USDT. They don’t know you swapped it for BTC. They don’t know what wallet that BTC ended up in. And most importantly, the government database has no record of you holding Bitcoin.

The end result: You hold BTC with no paper trail connecting it to your government-verified identity. Not illegal. Not money laundering. Just privacy—the way financial transactions worked for literally thousands of years before the surveillance state decided every transaction needed to be monitored.

This isn’t about hiding from taxes when you sell (you still owe those). This is about protecting your holdings from being targeted before you ever sell.

The Philosophical Foundation: Freedom vs. Permission

Let’s zoom out for a moment, because this isn’t really about cryptocurrency.

It’s about a fundamental question: What does freedom mean if you have to ask permission to exercise it?

The sovereign individual thesis—articulated most clearly by James Dale Davidson and William Rees-Mogg in their 1997 book The Sovereign Individual—argues that we’re entering an era where individuals can, for the first time in history, truly escape the monopolistic control of nation-states. Not through revolution. Through technology.

Cryptocurrency is one expression of this shift. Encrypted communication is another. Remote work that transcends borders is another. These aren’t just tools—they’re exits from systems that demand compliance in exchange for survival.

But here’s the philosophical trap that catches well-meaning people every single time: the difference between protection and evasion.

Evasion is avoiding obligations you legitimately owe.

Protection is defending yourself from obligations that haven’t been established yet—or shouldn’t exist in the first place.

When you don’t declare your self-custodied Bitcoin to the French government, are you evading taxes? No—because you haven’t sold anything. You haven’t realized a gain. You’re just holding property. When you eventually sell, you pay capital gains on the profit. That’s fair. That’s legitimate. If you think so.

But when the government demands you register that property just for holding it—not for selling it, not for profiting from it, but simply for possessing it—they’re not protecting society. They’re building infrastructure for future confiscation.

History is unambiguous on this point. Registration precedes restriction. Every. Single. Time.

The moral distinction matters here because this isn’t a case of “taxation is theft” libertarian absolutism. This is a case of recognizing that some demands for compliance are themselves illegitimate, regardless of whether they’re legal.

In 1850, the Fugitive Slave Act made it illegal to help escaped slaves. The law mandated that citizens assist in the capture and return of freedom seekers, with fines of $1,000 (roughly $37,000 today) for anyone who harbored escapees. Compliance with this law meant participating in the perpetuation of slavery. Violation meant choosing moral duty over legal obligation.

The people who violated that law weren’t criminals. They were protecting human beings from an unjust system. The law was illegitimate—not because it wasn’t enforced, but because no government has the legitimate authority to demand you participate in others’ oppression.

The parallel to crypto declaration laws isn’t perfect—we’re talking about property rights, not human freedom. But the principle holds: A law demanding you create the infrastructure for your own future persecution is illegitimate, regardless of its legal status.

You don’t owe the government a roadmap to your financial life. You don’t owe them a database of confiscatable assets. You owe them taxes on realized gains—nothing more.

The question isn’t whether you’ll comply with today’s laws. It’s whether you’ll architect your holdings to survive tomorrow’s.

What Comes Next

Here’s what I know: The surveillance net is tightening. France won’t be the last country to mandate crypto declarations. The regulatory creep will continue because governments have discovered that compliance is cheaper than enforcement. Why raid houses looking for gold when you can just consult the registry?

But here’s what else I know: The tools to resist this exist right now. The technology to sever the connection between your identity and your holdings is mature, tested, and accessible. You don’t need to be a cryptography expert. You don’t need to be a criminal. You just need to understand that privacy isn’t given—it’s taken.

Every generation faces a moment where they have to choose between convenient compliance and uncomfortable freedom. This is ours.

The question isn’t whether governments will try to control cryptocurrency. They already are. The question is whether you’ll design your financial life to require their permission—or whether you’ll build sovereignty into your architecture from the beginning.

France’s declaration mandate is just the opening move. But you don’t have to wait to see how the game ends.

You can opt out now.

Share This

If this resonated with you, share it with someone who’s still trusting the system to protect them. The conversation we’re not having is more dangerous than the one we are.